A farmer has successfully harvested his first crop of the season. He faces a daunting question—should he plant a second crop?

On the one hand, planting a second crop could yield additional income, capitalizing on the remaining growing season. If conditions remain favorable, this decision could fortify his earnings, setting him up for not just a prosperous year but also providing additional capital to invest in new equipment or technologies that could make future farming more efficient.

On the other hand, there’s a risk. Planting a second crop and then losing it to frost could result not only in a financial loss for the seeds but also in wasted labor and other resources.

Much like the farmer, investors also find themselves at a crossroads where they must determine the appropriate level of risk to assume. Just as the farmer must consider weather conditions, seed availability, and labor cost, investors have a myriad of variables to contemplate. These can range from market volatility, interest rates, geopolitical events, and individual company performance.

What Farming Has To Do With Investing

The farmer’s story illustrates an essential investment principle—risk and reward are often two sides of the same coin. One of the biggest challenges that investors face is determining the appropriate level of risk to take on.

On one hand, taking on too much risk can lead to devastating losses and financial ruin.

On the other hand, avoiding risk altogether can result in missed opportunities and suboptimal returns.

The equity risk premium (ERP) is a key concept that investors must understand to make informed investment decisions. However, there are many different opinions about what constitutes an appropriate ERP and how it should be calculated.

In this blog post, we will explore the various factors that contribute to ERP and offer insights into how investors can use this information to their advantage.

What is the Equity Risk Premium?

The equity risk premium is a way to measure the excess return that an investor expects to receive from holding a risky asset, such as stocks, over the risk-free rate of return. In other words, it is a measure of the compensation that investors demand for taking on the additional risk associated with investing in equities.

How do you calculate the Equity Risk Premium?

You calculate the Equity Risk Premium by using two components.

The first component is the earnings yield on a broad market index.

The second component is the risk-free rate.

Usually, a short-term U.S. treasury yield is used in the computation because the chance of the US government going bankrupt is practically nil due to the power of taxation and the money supply.

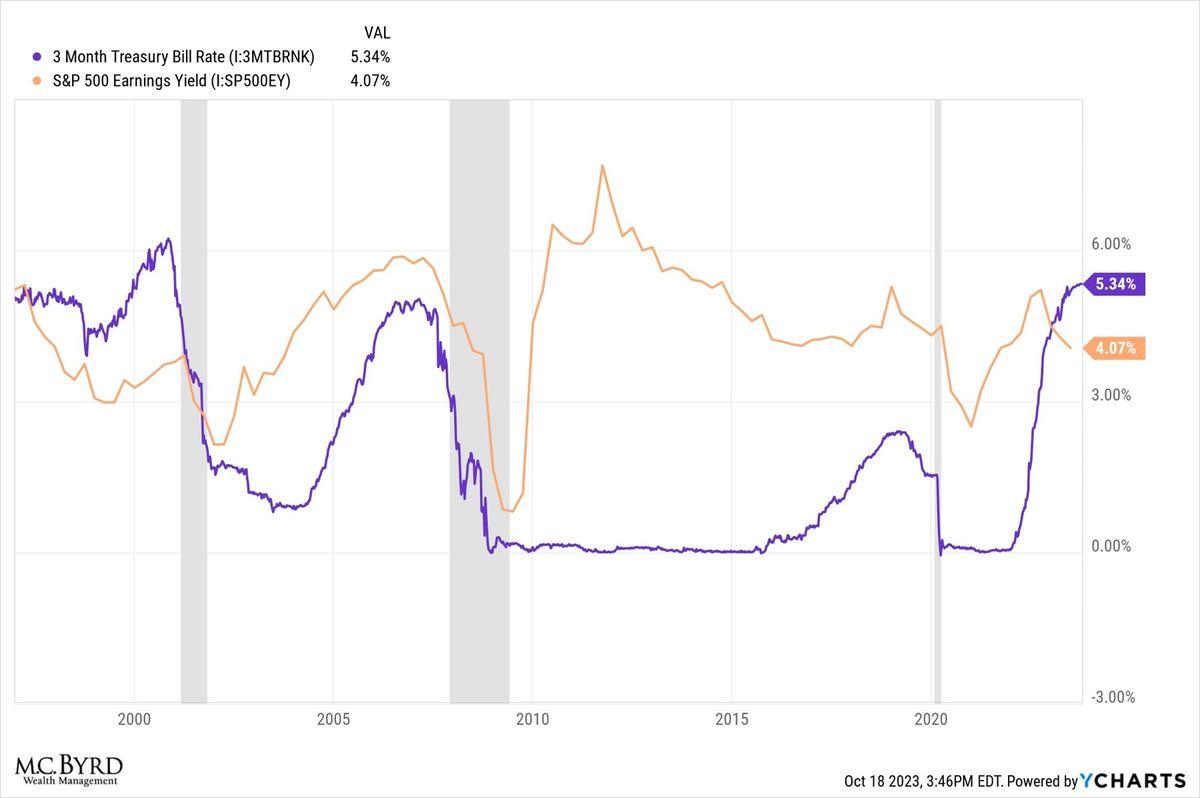

Where Is Equity Risk Premium Today?

The current earnings yield of the S&P 500 (a broad market index) is approximately 4-4.5%.

This includes the dividend that you earn while holding the S&P 500 plus the net profit that the S&P 500 stocks retain.

Let’s use the 90-day treasury bill for our risk-free rate. It is currently paying 5.35 percent.

Subtracting the S&P 500 earnings yield from the T-Bill yield produces a negative number.

In other words, an investor is not being paid for the risk of holding securities.

How often is the equity risk premium 0 or negative?

The last time the equity risk premium was negative was in the late 1990s and early 2000s.

TINA & Why Equity Risk Premium Is Important

ERP is an extremely important concept for both stock and bond investors.

Stocks and bonds compete for investors’ capital.

During the easy monetary policies of the last 23 years, interest rates were kept artificially low by the Federal Reserve.

This caused some investors to take on unnecessary risk.

The market developed an acronym for this situation, TINA (There Is No Alternative).

Due to the government’s monetary response to COVID-19, inflation was produced, and the Federal Reserve was forced to become an inflation fighter by raising interest rates.

Higher interest rates mean, for the time being, TINA is dead, as short-duration bonds present an attractive alternative.

Why doesn’t the market rotate entirely from stocks to bonds?

There are several reasons why you don’t have a massive rotation.

Some may assume that the treasury rates will fall and a premium will be restored.

Other investors may be in a position where a capital gain tax could prevent them from massively reallocating their portfolios.

Finally, an investor might believe corporate profits could improve, raising the earnings yield.

What happened last time rates were this high?

The last two times the Federal Reserve tightened financial markets and dried up liquidity through interest rate hikes of this magnitude, a recession followed shortly thereafter, causing markets to tumble roughly 50 percent.

As we enter a familiar season, negative equity risk premium is definitely worth paying attention to.